The Internet's Missing Payment Layer is Finally Being Built

AI agents may have solved the 30-year-old problem the internet was supposed to fix from the start

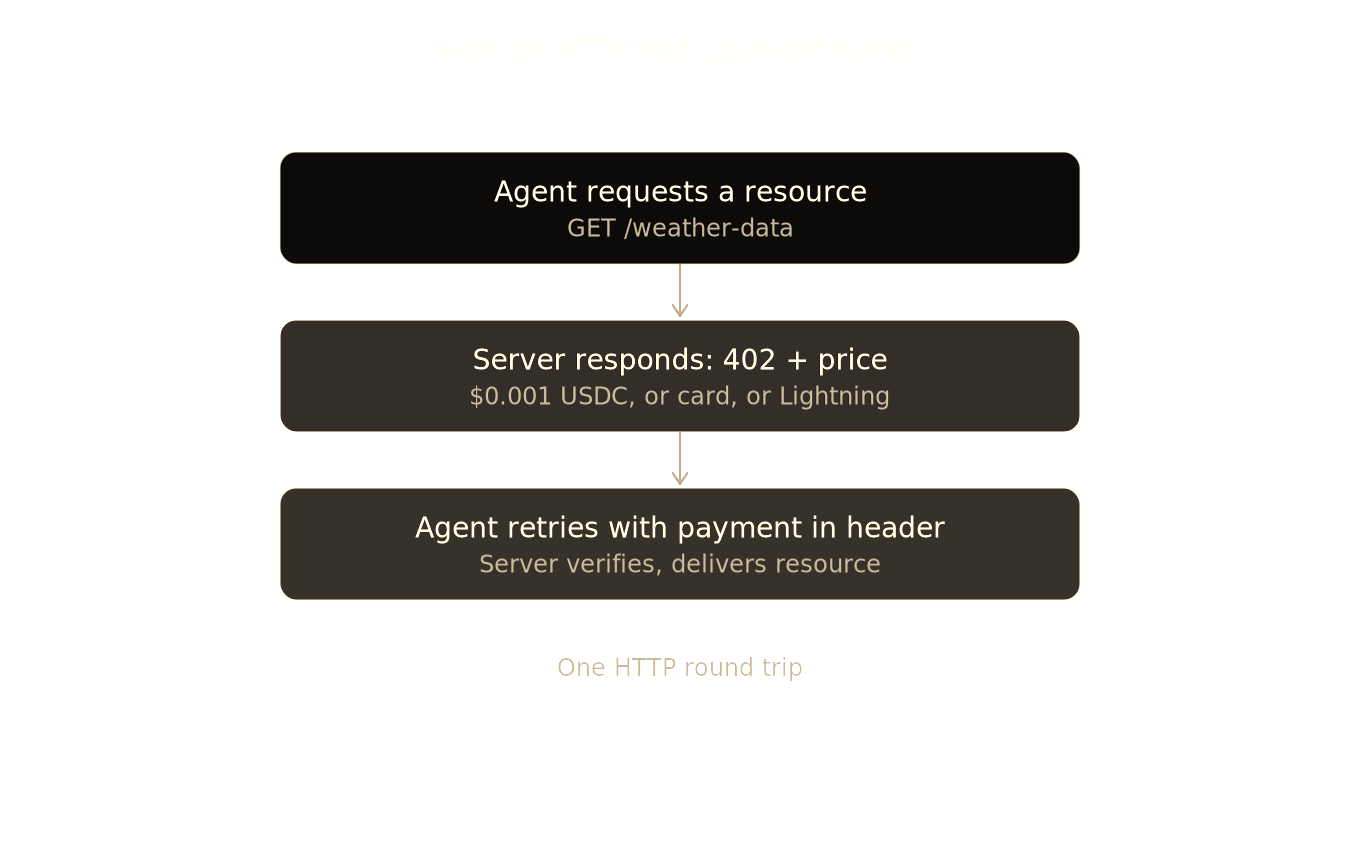

When the architects of HTTP were writing the spec in the mid-1990s, they buried a placeholder: status code 402, “Payment Required.” The idea was that a server could respond with a price, a browser could send payment, and the resource would be delivered. One round trip. Payments as native to the web as loading an image.

It never happened. The code sat dormant for nearly three decades. The internet chose advertising instead.

Now, two major protocols have revived HTTP 402. And the reason they might succeed where every prior attempt failed has less to do with technology and more to do with who the buyer is.

Micropayments Have a 30-year Track Record of Failure

A micropayment is a financial transaction small enough to be impractical through traditional payment rails. Fractions of a cent for an API call, a few cents for a single article, a thousandth of a dollar for a database query. The vision was always a third business model for the internet beyond advertising and subscriptions: pay only for what you use.

IBM and Compaq had micropayment divisions in the late 1990s. The World Wide Web Consortium (W3C) explored embedding payment tags into HTML. Companies like DigiCash, Millicent, and CyberCoin all tried. Every single one failed.

In 2003, Clay Shirky articulated what computer scientist Nick Szabo had earlier called “mental transaction costs”: the cognitive effort required to decide whether something is worth buying, regardless of price. A newspaper feels worth a dollar. But is each article worth half a penny? Shirky argued that beneath a certain price threshold, the mental effort of deciding whether to pay actually increases, because the value becomes harder to assess. That creates a floor on inconvenience that no amount of price reduction can remove.

This insight proved durable. Humans pause before spending money. They evaluate. They hesitate. And that hesitation, multiplied across millions of tiny transactions, kills the economics. Credit card processing fees reinforced the problem. A $0.30 fee on a $0.05 payment doesn’t work for anyone. Even as blockchain and fintech lowered those costs, the psychological barrier remained the harder problem to solve.

The Buyer is no Longer Human

AI agents are increasingly capable of autonomous work across multiple services. But when an agent needs a premium data feed, a GPU burst, or access behind a paywall, it hits checkout flows designed for people with eyes and fingers and credit cards. The work stops. A human has to step in.

Agents have no mental transaction costs. They don’t evaluate whether $0.001 is a fair price. They don’t abandon carts. They execute payment as a function call and continue working. The cognitive friction that killed micropayments for three decades does not apply to a non-human buyer.

Two Protocols, More Complementary than Competitive

x402, developed by Coinbase, went live in May 2025 as the first protocol to give HTTP 402 an actual implementation. A client requests a resource, the server responds with a 402 and payment instructions, the client submits payment in an HTTP header, and the resource is delivered. Settlement runs through a “facilitator” handling blockchain complexity, currently supporting USDC on Base, Solana, and Polygon. The x402 Foundation, co-founded with Cloudflare, now includes Google and Visa. Since launching on Solana, x402 has processed over 35 million transactions and $10M+ in volume. It was born crypto-native. Fiat support is on the roadmap but not yet live.

MPP (Machine Payments Protocol), co-authored by Stripe and Tempo, launched on March 18, 2026. It covers the same core flow but makes different architectural choices: no facilitator requirement (payment extensions are written directly into the spec), a “sessions” primitive for high-frequency micropayments (an agent deposits funds upfront and issues vouchers per request, settling in a single transaction at the end), and fiat support from day one via Visa, Lightspark (Bitcoin Lightning), and Stripe’s existing card infrastructure. MPP’s spec has been submitted to the IETF for formal standardization. Over 100 services were live at launch, with partnerships spanning Anthropic, OpenAI, DoorDash, Mastercard, Revolut, and Shopify.

MPP is backwards-compatible with x402. The two protocols serve different segments of the same emerging market: x402 has production history and crypto-native infrastructure, MPP has fiat flexibility and Stripe’s distribution. This dynamic could shift as both mature, but for now, they are building on each other rather than against each other.

What This Could Look Like in Practice

These use cases are hypothetical, but they illustrate the types of transactions these protocols are designed to enable.

You ask an AI agent to summarize the best reporting on a developing story. It hits paywalls at three publications. Instead of three subscriptions, it pays a few cents per article for only the pieces it needs.

A DeFi agent monitoring yield opportunities across multiple chains needs real-time pricing data from on-chain analytics providers and a risk scoring API to evaluate protocol exposure. Each query costs fractions of a cent, paid per call, with no API key registration or monthly commitment required.

The common thread: situations where the current alternatives are an expensive subscription you underuse, a procurement process that takes longer than the task itself, or simply going without.

The Market

McKinsey projects agentic commerce could generate $3 trillion to $5 trillion in global revenue by 2030, with up to $1 trillion in U.S. B2C retail alone. Morgan Stanley estimates $190 billion to $385 billion in U.S. e-commerce through agents by 2030, representing 10% to 20% of online retail. These figures reflect goods only and do not include services, where much of the micropayment activity will likely concentrate.

That said, these projections model a future that has not arrived yet. Only about 1% of shoppers currently use any form of agentic purchasing. The infrastructure is being built ahead of mass adoption.

Several risks deserve honest attention. Regulatory frameworks for agent-initiated purchases are undeveloped. And the settlement rail question remains open: if most agent commerce flows through traditional card rails, Stripe and MPP have the structural advantage; if stablecoin-native settlement dominates, Coinbase and x402 got there first.

What to Watch

Transaction volume. Actual throughput on x402 and MPP networks, measured consistently over time. x402 has 35M+ transactions. MPP launched with 100+ services. These are starting points. The signal that matters is whether those numbers compound quarter over quarter, or plateau once the initial wave of early adopters integrates.

The IETF standardization process. If MPP’s spec is adopted, it would mark the first time HTTP 402 has had a formal implementation in the 30 years since it was created. That would be a structural milestone for the entire space, giving MPP the weight of an official internet standard.

How settlement splits between fiat and crypto. This is the question that will shape how the industry consolidates. If agents predominantly settle through card rails, value accrues to Stripe, Visa, and the existing payments infrastructure. If stablecoin-native settlement wins, it accrues to Coinbase, blockchain L1s, and the facilitator ecosystem built around x402. Early signals suggest both will coexist, but the ratio matters enormously.

The internet was designed to move information seamlessly. It was never given the ability to move money the same way. Thirty years later, the status code that was supposed to fix that is finally being put to use. The difference this time is that the customer placing the order doesn’t need to decide whether it’s worth it.

Sources:

Coinbase, “x402: A payments protocol for the internet”, GitHub

Stripe, “Introducing the Machine Payments Protocol”, March 2026

Cloudflare, “Launching the x402 Foundation”, December 2025

Visa / PYMNTS, “Visa Teams With Stripe on Agent Payments”, March 2026

McKinsey & Company, “The agentic commerce opportunity”, October 2025

Morgan Stanley, “Agentic Commerce Impact Could Reach $385 Billion by 2030”

Clay Shirky, “Fame vs Fortune: Micropayments and Free Content”, 2003

Forrester, “Why Stripe’s MPP Signals A Turning Point For Micropayments”, March 2026

AWS, “x402 and Agentic Commerce”, March 2026